It Is An Expense For Leased Office Space Equipment Or Assets Rented From Others. Leases with a base value with low replacement value. So if a company leases an office for a short period of time, it does not have to be accounted for. assets in lease accounting represent the right to use leased items or properties, classified based on various factors such as convertibility, physical. Common examples of leased assets would be: a lease agreement is a contract between two parties, the lessor and the lessee. in summary, calculating equipment leases under asc 842 requires determining the present value of lease payments using the company’s ibr and. Leases with a term of less than 12 months, without an option to purchase. ifrs 16 similarly defines a lease as “a contract, or part of a contract, that conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration.” so what is a leased asset? it will not be wrong to say that the accounting for an equipment lease (financial or capital lease) is similar to accounting for any fixed asset. exemption from ifrs 16 for office space under this new regulation, two exemptions are granted: The lessor is the legal owner of the asset, the lessee.

from freeforms.com

a lease agreement is a contract between two parties, the lessor and the lessee. ifrs 16 similarly defines a lease as “a contract, or part of a contract, that conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration.” so what is a leased asset? Leases with a base value with low replacement value. Common examples of leased assets would be: exemption from ifrs 16 for office space under this new regulation, two exemptions are granted: it will not be wrong to say that the accounting for an equipment lease (financial or capital lease) is similar to accounting for any fixed asset. The lessor is the legal owner of the asset, the lessee. assets in lease accounting represent the right to use leased items or properties, classified based on various factors such as convertibility, physical. in summary, calculating equipment leases under asc 842 requires determining the present value of lease payments using the company’s ibr and. So if a company leases an office for a short period of time, it does not have to be accounted for.

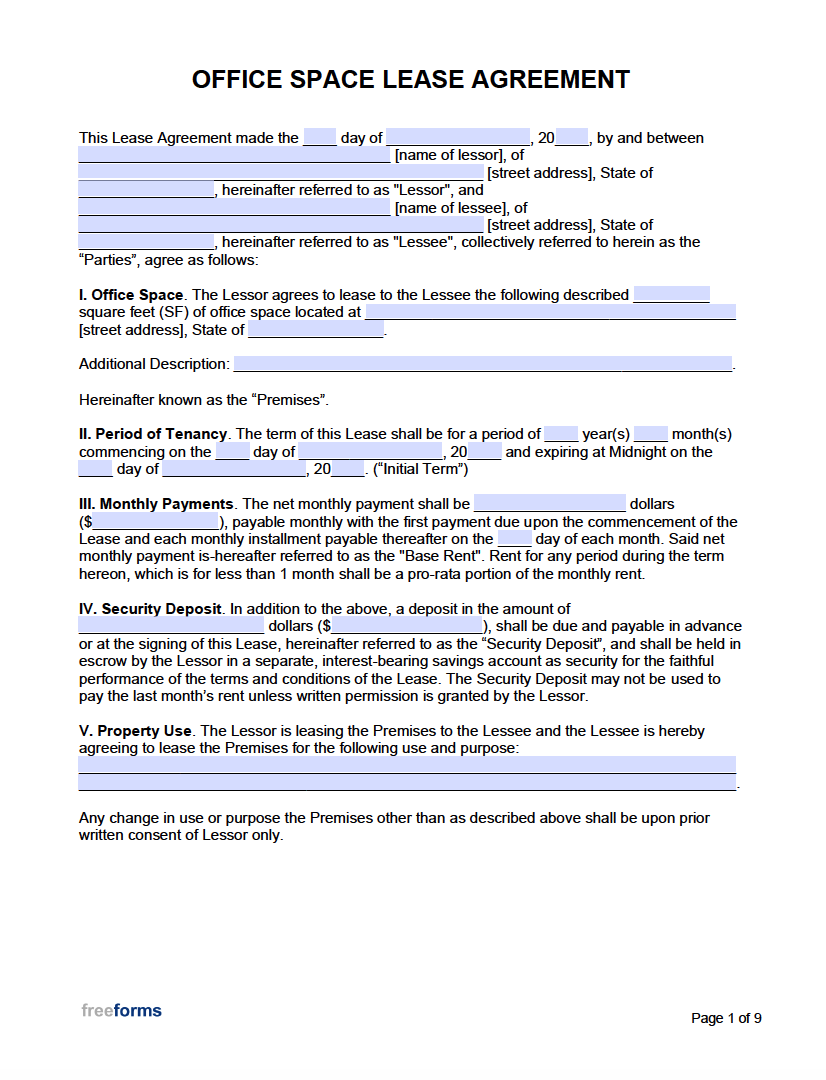

Free Office Space Lease Agreement PDF WORD

It Is An Expense For Leased Office Space Equipment Or Assets Rented From Others So if a company leases an office for a short period of time, it does not have to be accounted for. it will not be wrong to say that the accounting for an equipment lease (financial or capital lease) is similar to accounting for any fixed asset. a lease agreement is a contract between two parties, the lessor and the lessee. Common examples of leased assets would be: in summary, calculating equipment leases under asc 842 requires determining the present value of lease payments using the company’s ibr and. So if a company leases an office for a short period of time, it does not have to be accounted for. The lessor is the legal owner of the asset, the lessee. Leases with a base value with low replacement value. ifrs 16 similarly defines a lease as “a contract, or part of a contract, that conveys the right to use an asset (the underlying asset) for a period of time in exchange for consideration.” so what is a leased asset? assets in lease accounting represent the right to use leased items or properties, classified based on various factors such as convertibility, physical. Leases with a term of less than 12 months, without an option to purchase. exemption from ifrs 16 for office space under this new regulation, two exemptions are granted: